Bernanke's actions last week - failing to taper, yet still trying to maintain the illusion that QE is a good thing - are setting up a one-two punch that's not unlike boxing champion Mohammed Ali's famous "float like a butterfly, sting like a bee" approach.

If you recall, Ali was a master of the combination - some say the best ever. He loved to bring his opponents in close. Ali could see through the duplicity of his opponents' strategy and land punches that won decisively.

Ali did that using combinations that were based in fighting terms on two contrasts: high-low or short-long, or even left and right. He pressed every advantage he could find, even when others thought there were none to be had. Knowing he wanted to go the full 15 rounds, Ali developed a strategy that would become known as the "rope-a-dope" as a means of tiring out his opponents early on, then vanquishing them in later rounds when the fight really began.

I think we should take a page from Ali's playbook and split the "fight" Bernanke's presented us with into two distinct time zones: the current "round," and those that happen down the line. One short. One long.

Is that possible?

Absolutely. What's more, it's easy to do.

First, though, put yourself in Bernanke's place...

Losing His "Final Round" Would Crush You, the Markets, and Bernanke HimselfFor all the lip service he pays to wanting growth, in reality, Bernanke's game is all about defense... from the moment he wakes up to the moment he goes to bed.

Why is pretty simple.

Right now, he has to keep a lid on everything from the looming budget battle to the Middle East. His risk is that the consumer gets crushed if he doesn't. So he's going to keep buying, lest he create a market crash that goes down on his watch, destroying his reputation and vaporizing the rumored $10 million advance for his memoir.

Longer term, he's got trillions of reasons why he doesn't want to pop the bubble, the most important of which is that he doesn't want to lose control over the bond markets and, by implication, interest rates.

The rub is that he will anyway. And I think Chairman Bernanke is acutely aware of that now, because derivatives traders are beginning to circle like sharks sensing blood in the water.

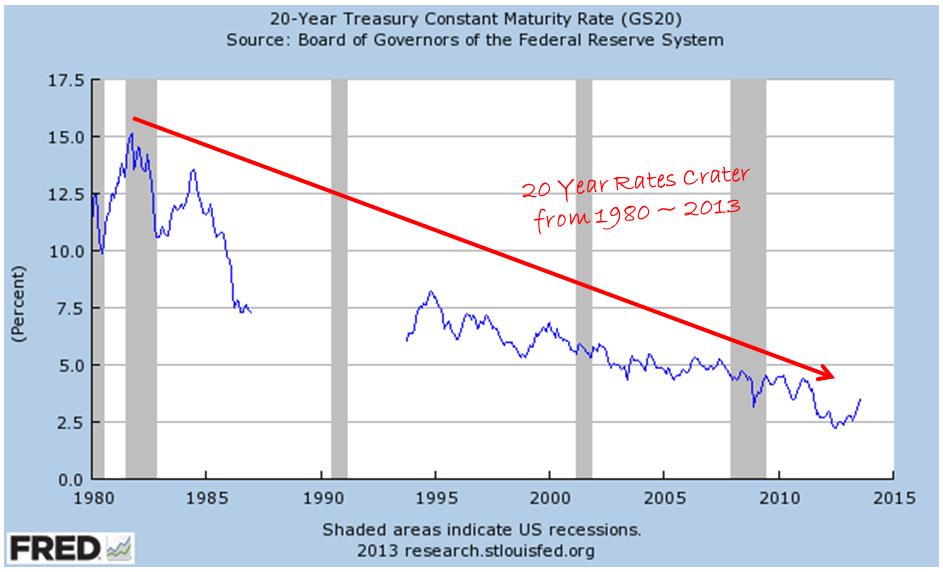

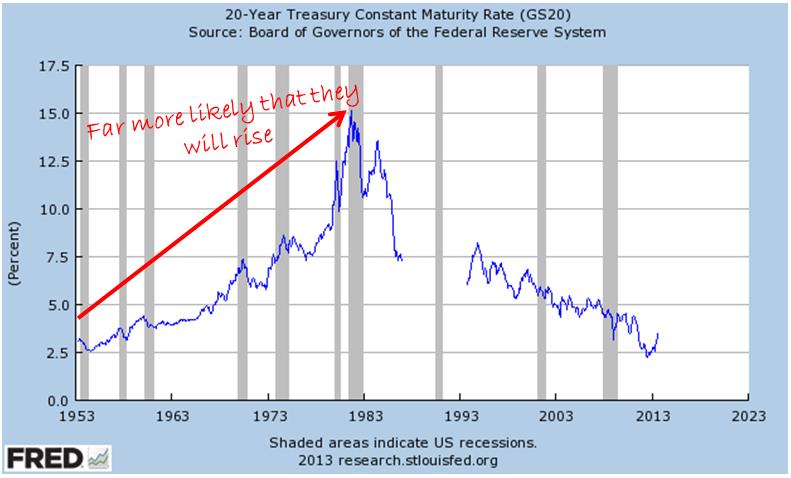

Factor in trillions of dollars, and there's enough fuel to drive rates higher for decades after he's gone, especially if you look at how far rates have fallen.

Since 1981, they've plummeted from 15% to a mere 3.46%, as of Monday.

The far more likely course of action is that they rise like they did from 1950 to 1981... especially when you look at the bigger picture and understand that interest rates move in multi-decade cycles.

(By the way, if you're wondering why there's no data from January 1, 1987, through September 30, 1993... The Fed discontinued the 20-year constant maturity series at the end of the calendar year 1986 and reinstated the series on October 1, 1993.)

A One-Two Investment Approach1. For the near term, try the Pimco Strategic Global Government Fund (NYSE: RCS).

Managed by Allianz Global Investors Fund Management LLC, the fund is constructed of intermediate-term, high-quality government securities. The fund can invest in mortgage-related and asset-backed securities, too, if managers so desire. It's also got the flexibility to pick up foreign paper.

The dividends are paid monthly, which means that income-hungry investors will get cold, hard cash in their accounts regularly. That's not insignificant, considering the yield is a healthy 9.2% as of press time, according to Allianz.

2. For the longer term, I can't think of a better pick than the ProShares Short 20+ year Treasury (NYSE Arca: TBF).

This ETF is one of a specialized class of inverse funds that zigs when the universe around which it's constructed zags. In this case, TBF is designed to appreciate while longer-term U.S. bonds deteriorate.

As its name implies, the fund concentrates investments in U.S. Treasury securities with maturity dates longer than 20 years. That's great, because longer-dated maturities are the most volatile in the face of rising interest rates and, therefore, potentially offer some really great returns.

There's no yield, and the 0.95% in expenses doesn't make this the cheapest alternative out there, but I like the liquidity afforded us by the $1.47 billion in assets. It's also unleveraged, which means that performance-reducing tracking error that plagues similar double- and triple-leveraged funds is minimized.

At the end of the day, it's important to remember that interest rates will return to normal sooner or later, and these two investments will help you capture profits that can be yours for the taking when they do.

You don't have to play defense even if Bernanke does.

Best regards for great investing,

Keith

P.S. If you're wondering about equities, I'll be back in a few days with my take. But here's a hint if you just can't wait: Equities remain under-owned compared to bonds - this despite a 135% run up off March 2009 lows, and despite Bernanke's near laser-like focus on cheap money. So there's an incentive for the institutions to lever up even further and, in the process, goose stock market returns through the balance of the year. I know that with the S&P 500 and Dow waffling this week that this is hard to imagine, but don't forget - so was the concept of trillions of dollars of stimulus a few years ago.

Next: "The Secret to Superior Returns," where Keith shares one of the key strategies driving his Money Map Report's outstanding total return...